Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

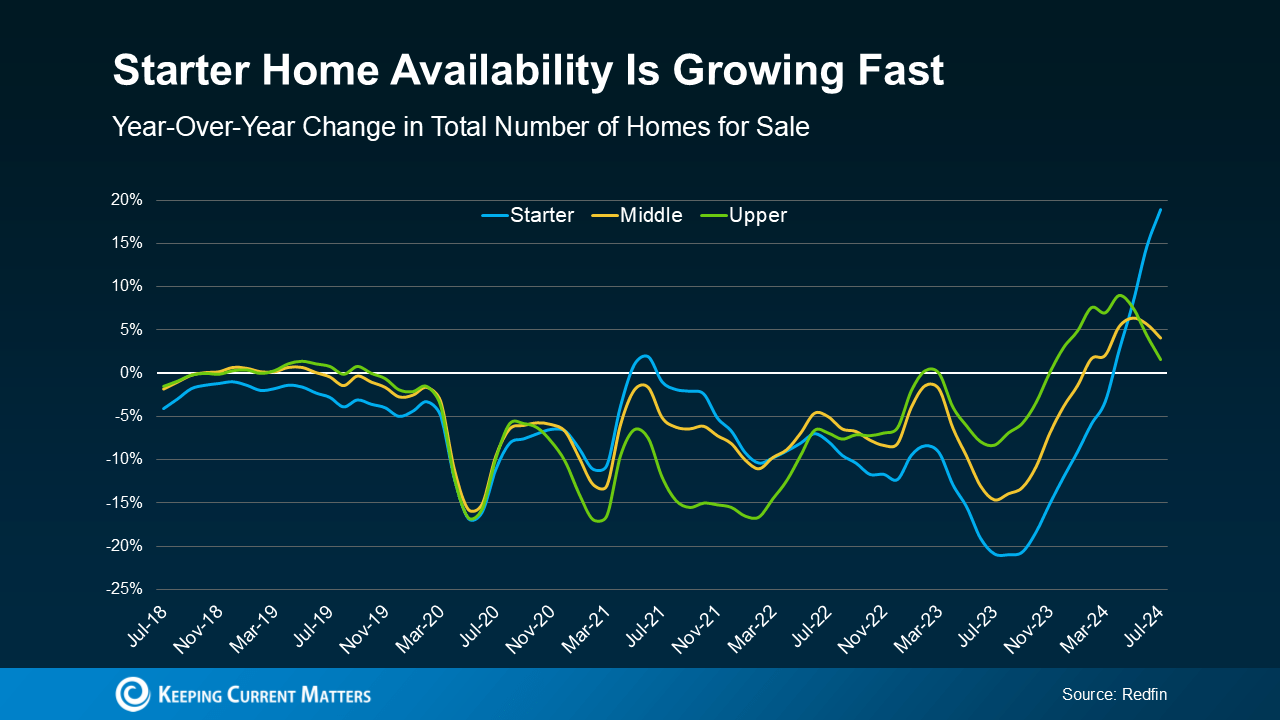

More entry-level homes – also known as starter homes – are popping up on the market. And after several years with very few homes available to buy and prices rising, there are finally some more options for first-time buyers.

Inventory Is Increasing – Especially at Lower Price Points

Over the past year, the total supply of homes for sale has improved. According to Realtor.com, in November there were 26.2% more homes for sale compared to this time last year, marking 13 months of inventory growth and the most homes available since December of 2019.

Interestingly, the growth isn’t spread evenly among all types of homes, though. According to Redfin, starter homes have seen the biggest increase (see graph below):

So, if you’re a first-time buyer who’s been sitting on the sidelines waiting because you thought you might never find a starter home in your market, this could be a game-changer. You finally have more options to choose from, and you just might be able to find one in your price range.

So, if you’re a first-time buyer who’s been sitting on the sidelines waiting because you thought you might never find a starter home in your market, this could be a game-changer. You finally have more options to choose from, and you just might be able to find one in your price range.

How an Experienced Agent Helps You Find a Starter Homes

Finding the right starter home at the right price point in your local market might feel like an unthinkable challenge, but a local real estate agent makes it easier. They stay up to date on the latest starter home listings in your area, so you don’t miss any opportunities.

Your agent will help you focus on homes that match your budget and your needs, making the search less stressful. They’ll also guide you through how to make the right offer and negotiate to get the best outcome possible.

On top of that, they handle the important details, like documentation and deadlines, so you can stay right on track. And if you have questions, your agent is there with answers and expert advice every step of the way.

Bottom Line

Starter homes are making a bit of a comeback, and this could be your chance to find one. Whether you’re ready to visit listings, need advice, or just want to see what’s out there, reach out to a local real estate expert.

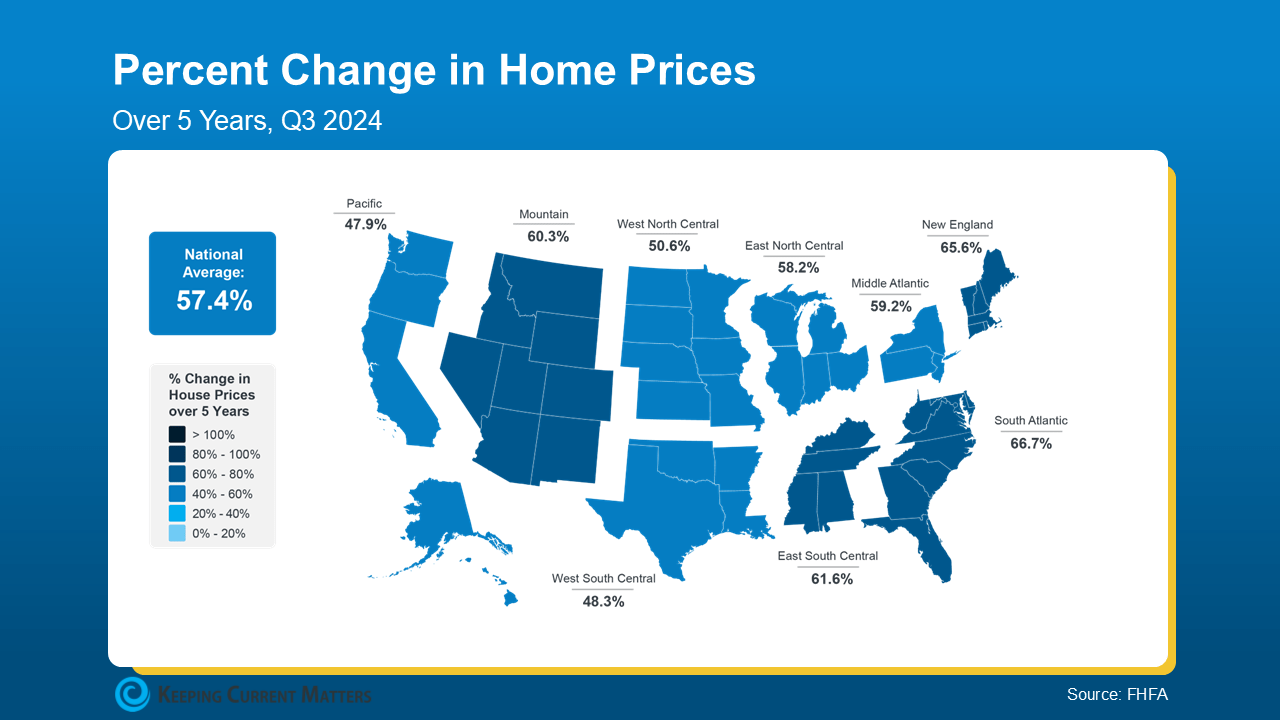

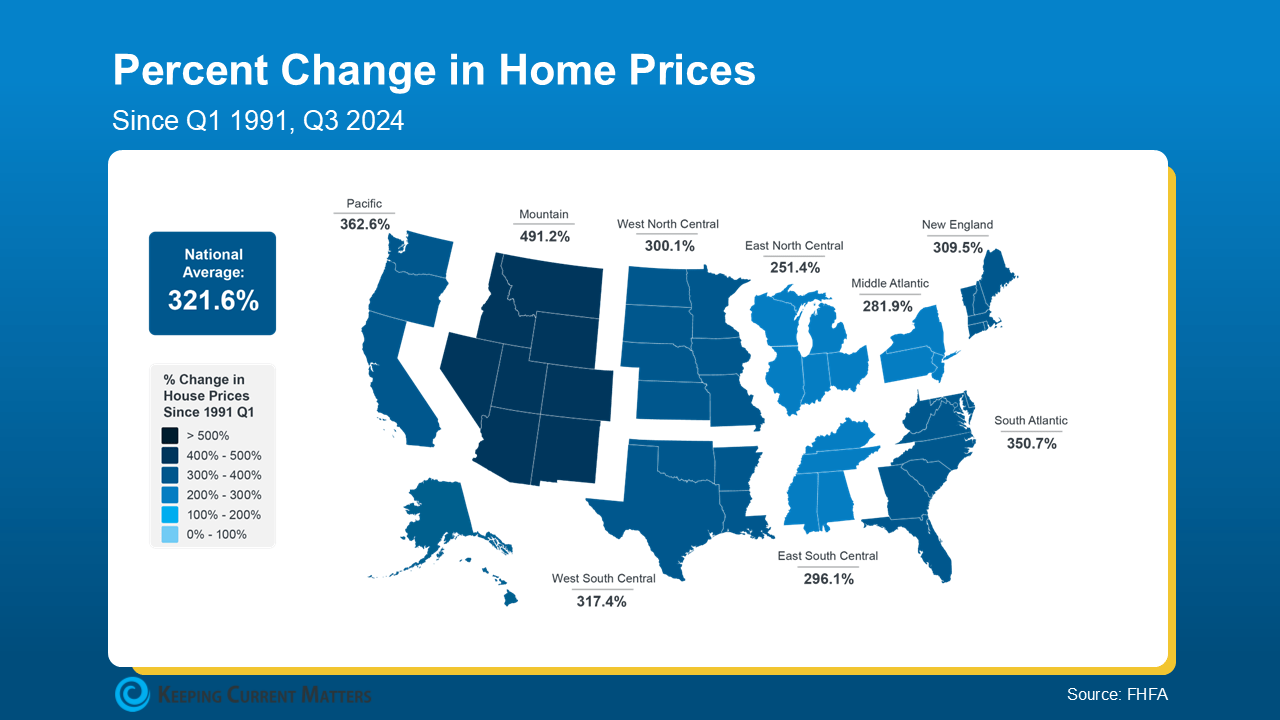

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.

The second map shows that, over a roughly 30-year span, home prices appreciated by an average of more than 320% nationally.